Survey results — Travel industry outlook after CV19

These results shed some light on the expected impact on various travel categories and competitors as well as the new opportunities for…

These results shed some light on the expected impact on various travel categories and competitors as well as the new opportunities for travel companies

Route 50. The Loneliest Road in America (Photo by Mauricio Prieto)

Last week I sent out a survey covering the post CV19 travel environment and addressing the following topics:

Travel categories — relative winners and losers after CV19

Individual competitors — relative winners and losers

Estimation of travel activity in 6, 12 and 24 months

Main long standing impact on the travel industry

Main opportunities for startups

Previous biggest travel mega-trends that make less sense after CV19

I sent the survey to two groups:

Group A was a selected group of travel industry professionals that I handpicked to represent a wide variety of travel categories across geographies. 26 people completed the survey in this group.

Group B. Individuals that receive my Travel Tech Essentialist newsletter, sent every two weeks with my pick of the 10 top stories in travel tech. In my most recent issue I included a link to the survey. 39 people completed the survey.

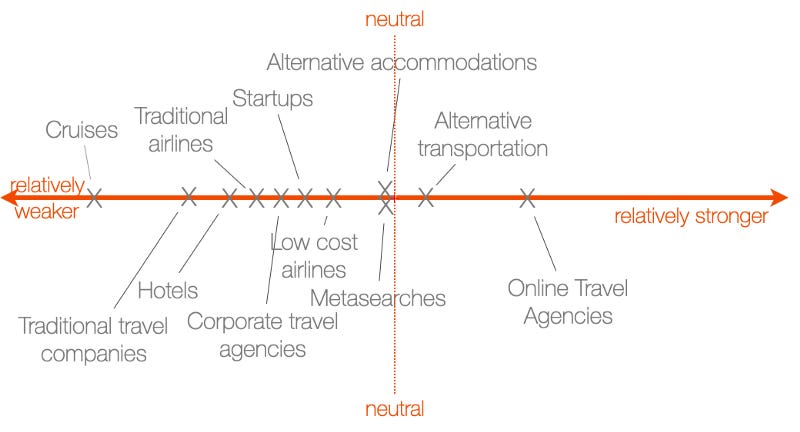

Question 1: Which will be the relative winners and losers emerging after CV19?

Options: Relatively weaker, neutral, relatively stronger.

It is clear that this crisis will affect every player in a negative way, but this question seeked to address who will be *relatively* worse or better off compared to other players in the industry.

Question 1 for Group B had a few additional categories that were not in Group A’s: Cruises, traditional airlines, low cost airlines, traditional travel agencies.

In order to have a visual of the results in a numbered line, I did a weighted average for each answer, where “weaker” = 0, “neutral” =1, “stronger” = 2.

Group B’s answers were generally more optimistic than Group A’s. Group A did not have any travel category with a weighted average above “neutral”.

Both groups had the same top 4 travel categories: Online Travel Agencies, alternative transportation, alternative accommodations, metasearches. This points to a belief that intermediaries and companies that have an asset-light model could have an edge after the crisis. Within the same category, the level of confidence increases with the more digital native companies. For example, OTAs are rated relatively stronger than traditional travel agencies; similar for alternative accommodations versus hotels and for low cost versus legacy airlines. It is worth noting that alternative transportation is believed to be the relatively strongest in Group A and second strongest in Group B. This makes sense as travellers seek transportation alternatives to air travel both for perceived health-related benefits and also for convenience of multimodal transportation.

On the weakest end of the spectrum, there is some consensus that traditional suppliers, companies most exposed to business travel and startups that might not have solid cash positions will have a tougher time after CV19. Group A had corporate travel management companies, startups (certainly too generic of an option) airlines and hotels. Group B had cruises, traditional travel companies, hotels and traditional airlines.

Results: Question 1 Group A

Which will be the relative winners and losers emerging after CV19? Weighted average based on 26 responses for Group A.

Results: Question 1 Group B

Which will be the relative winners and losers emerging after CV19? Weighted average based on 39 responses for Group B. Group B had the following additional categories to complete than Group A: Cruises, traditional airlines, low cost airlines, traditional travel agencies

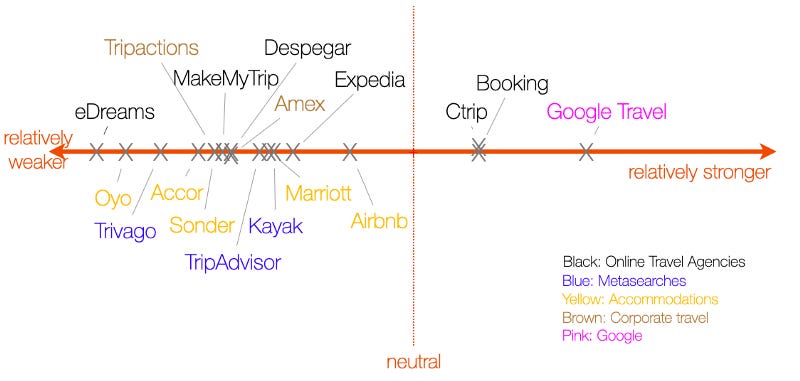

Q 2: Similar to Q1, but now specific to individual competitors

Zooming into individual competitors, Group B shows again more optimism, but Group A now has 3 companies in the positive half of the line.

Just like in question 1, in order to have a visual of the results in a numbered line, I did a weighted average for each answer, where “weaker” = 0, “neutral” =1, “stronger” = 2.

Both groups coincide in the 4 companies that will be relatively stronger than the rest of the field: Google Travel, Booking, Ctrip, Airbnb and Expedia.

In the OTA category, the six players are very spread out. There is a very significant difference between the perceived weakest (eDreams) and strongest (Booking), occupying the ends of the spectrum among the 17 competitors in the survey. Both groups had the same order for the six OTAs (from weaker to stronger): eDreams, MakeMyTrip, Despegar, Expedia, Ctrip and Booking. Flights focused regional OTAs are believed to be impacted more compared to global OTAs. This is an outcome I suggested in my previous post:

Hotels, airlines, OTAs and other travel players whose business is most reliant on emerging markets and developing economies will suffer a greater impact. Truly global intermediaries like Booking.com or Airbnb that do not have a high dependency on any single geography and can quickly and opportunistically redirect its business to the most promising geographies are better positioned to adapt than other OTAs that are more reliant on a particular country or region — Mauricio Prieto- A New Normal in Travel Post COVID19

Of the 5 players in the accommodations category, Oyo is seen as the weakest and Airbnb as the strongest by both groups. Sonder is the second strongest by Group B. The alternative accommodation product and platform model is perceived as better positioned out of the crisis.

Corporate travel seems to be an exception, since the traditional player (American Express Business Travel) is ranked higher than Tripactions, launched in 2015 with $480 million raised to date.

In metasearch, Trivago lags in both groups, with Kayak ahead in Group A and TripAdvisor in Group B. But all three players are in the negative half of the line.

And Google Travel, as always, seems to be in a league of its own. Group A had it as the best positioned by a good margin, and Group B had it second to Booking.

Results: Question 2 Group A

Which will be the relative winners and losers emerging after CV19? Weighted average based on 26 responses for Group A.

Results: Question 2 Group B

Which will be the relative winners and losers emerging after CV19? Weighted average based on 39 responses for Group B.

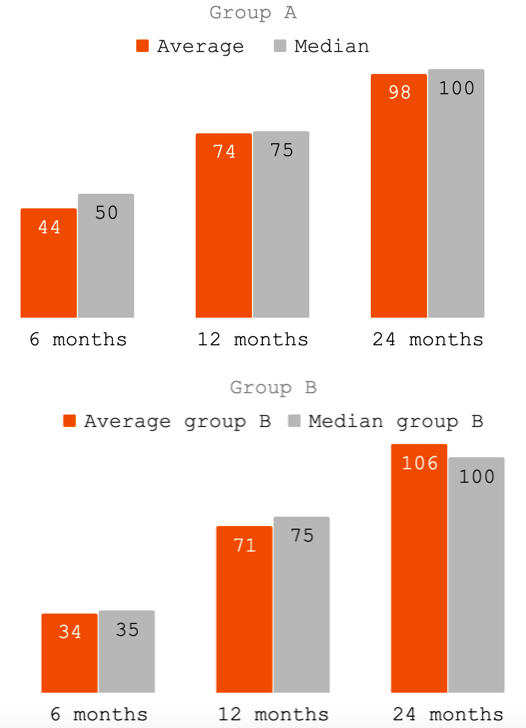

Q3: Indexing at 100 the previous “typical” travel volumes/activity of 2019, what’s your estimation of where this index will be in 6, 12 and 24 months?

For example, “50” would be half of typical/normal 2019, “200” would be twice as much, etc…

Group B is slightly less optimistic than Group A (contrary to the previous questions), with an expectation that travel activity in 6 months will be at 35% (median of responses) compared to 2019 versus 50% for Group A. In 12 months, the estimation for both groups is that we will be at 75% of “normal” 2019 travel activity, reaching 100% of 2019 activity in 24 months.

100 = 2019 travel activity. Where will we be in 6, 12 and 24 months? 26 responses in Group A; 39 responses in Group B.

Q4: What do you think will be CV19’s long standing impact on the travel industry?

See below in italics some of the representative responses made by survey respondents. I am dividing the responses between main themes.

Higiene / health

At its core, CV19 is a global health crisis and wake up call that we cannot take our health for granted. When we do return to travelling, our health and well-being will be top of mind with every decision. Travel providers and destinations who survive will emerge and win when they provide consumers with travel choices that promote health and well-being. This will include new levels of cleanliness, physical space and “touchless tech”. Insurance, health-tech and virtually every travel sector has an opportunity to innovate in this space. Corporate travel may not come back as fast as it has from previous crises given how hard many companies have been hit financially. Airbnb and other companies in that space may also be impacted if they don’t have a way to control standards for guests.

Focus on hygiene factors across the industry and more demand for non-massive destinations.

Sanitation measures for suppliers (airlines and hotels) will require new procedures and investment to adapt to new standards

Insurance / cancellations

Travellers’ behaviour will probably shift towards personal security. Until a vaccine is found, there’ll probably be a sharp uptake in insurance policies, as well as accommodation type changes (e.g., self-contained accommodation units vs shared living)

Insurance policies, flexible bookings, more bookings through agencies,

Intermediaries / suppliers

The war between direct/indirect business for hotels is less relevant now. First priority will be to get any bookings, whoever can do that will be a beloved partner, no matter the commission.

Strong market consolidation on supplier side for airlines, weaker airline intermediaries, accommodation intermediaries might become stronger due to lots of distressed inventory to sell, very few startups will survive.

Intermediaries who play well their cards and add value quickly will gain share (similar to 9/11 and other strong demand crises).

Guests will likely feel more protected by booking on intermediaries than directly. Reduction of direct revenue and drop of not-refundable rates. More flexibility on cancellations.

For suppliers, this is a great opportunity to build a closer relationship with travelers and decrease their dependency on OTAs.

The relationship between suppliers and retailers will be worse than ever especially with the airlines.

Airline concentration and a more direct approach between airlines and customers.

Corporate travel

Return of Duty of Care considerations by corporates and TMCs, greater appreciation to the need of corporations to look after travellers and higher concern with flight delays and cancellations and their impact on business continuity. Trying to minimize time spent in airports.

Business travel and events permanently altered as more meetings (both intra and inter company) go virtual at an accelerated pace.

Industry changes and dynamics

Main industry changes: 1) Corporate travel will go down; 2) Some airlines will shut down, there will be M&A activity; 3) Cost base of all travel entities will reset to a notch lower; 4) Reduction in marketing spend.

Air travel will become more cumbersome due to new hygiene and social distancing regulation.

Alternative accommodations and domestic trips made by car or train will grow because of more open space or a perception of safety. Also I think people will begin to travel to non typical destinations, they will avoid crowded cities.

Companies with weak balance sheets/strong indebtedness/strong fixed costs will go bankrupt or have to be bailed out by investors or governments.

Years of greatly reduced travel demand and oversupply. Many companies folding. Accelerated consolidation.

Short and medium term: boost in domestic travel. Long term: back to normal, except the cruise industry, permanently weaker

Cruises, Long haul and business travel will be extremely affected

Increased fragmentation in a broad sense due to more “purposeful” travel as world gets accustomed to tech-driven virtual experiences and all types of travelers hone in on what’s important to them — decreased biz travel (cost — unless absolutely necessary), greater environmental awareness, physical distancing/health risk impacting destination selection and type of travel.

Less air travel will lead to less flights, less congestion in airports, less accommodation in large cities. Hotel prices will drop as occupancy drops and demand from corporate travel weakens. Airbnb type inventory in cities will move to the long term rental market while rural inventory will become more lucrative. Price parity in US hotels will collapse as hotels focus on occupancy rather than own channel / maintaining control.

Airbnb/VRBO will rebound first; hotels will rebound second — airlines third — cruises last. We will have a bull market in stock market as these industries stabilize. Rebound will be 6–8 month — with full bull run in 8–12 months.

Corporations will have to build stronger balance sheets. This won’t be the last outbreak…

Consumer behaviour

More friction in the system and less consumer appetite will translate in less intercontinental travel, less group travel, more individualized tour, less corporate.

People will hold on leisure travel for longer than we think. The economic impact and job losses will strongly impact purchasing power in the short-mid term. Fear of a new surge in cases will prevent people from taking longer-haul flights. Alternative accommodation will gain share over traditional hotels as people will prefer to stay away from crowded places for some time.

Less leisure travel as income shrinks or at least is less secure and less money is available per household for optional spending (such as travel) and more money is saved due to increased insecurity.

Consumer behavior changes: 1) Average advance planning window for leisure travel could go down; 2) Customers start focusing more on cancellation policy when selecting fare type; 3) Customers might prefer individual accommodation (such as Airbnb) as against hotels to minimize risk of infection; 4) Europe might have a long term dent on international tourist inflows from outside Europe, as people continue to avoid countries that were most impacted by Coronavirus.

Being in isolation will make people more conscious of the things they care about the most. Social distancing will increase the emotional value of traveling. This is giving a lot of people a wakeup call on what they used to take for granted.

Travelers will enjoy their trip mores, even if it’s a weekend getaway, a single day trip or a multi-week trip with family/friends, people will be more mindful when traveling.

Tourism will not be seen by locals as just a business opportunity but also as a sanitary threat. Initiatives against tourism may increase.

Q5: Previous crises have also originated new innovations. What do you think are the main opportunities that travel startups will focus on after CV19?

See below in italics some of the representative responses by survey respondents.

Travel health/medical related startups. We might also see some startups focused on domestic markets and shorter trip durations. Travel and hospitality providers that can truly blend e-commerce with excellent customer service should also have a competitive advantage at scale; on the one hand, people want to buy products online but will demand high quality and timely customer service that they can access with travel advisors. On the corporate side, better duty of care products may also emerge as companies need to proactively track, notify and rebook travellers.

Travel was about finding experiences; now it will be about minimizing anxiety.

Rebooking apps and travel insurance will live a renaissance moment.

Standards around hygiene (similar to LEED certified) across the travel industry.

Consumer interest in Asia as a destination (given safety and treatment of virus) and waning interest in traditional European destinations (Italy, France, Spain).

Remote work becomes a standard corporate policy, and destination (e.g. Costa Rica) remote work facilities emerge.

Masks as essential wardrobe element. Everyone (not just Asians) wears masks in a plane / airport.

Innovation in conference design. What can only happen in person? Conferences get more expensive and more elaborate.

Customer service in crisis time; no travel industry player has gained trust from their customers in this crisis.

Data companies who are able to cater to the travel ecosystem providing actionable insights and enabling conversations between suppliers and end consumers

Duty of Care solutions, health and safety on the plane and in airports

There is an opportunity to improve quality/cost of “close to real” virtual meeting platforms.

Companies that are hyper-local will win on this one. So markets that are typically net senders (nordics, UK, Germany) will win tourism related to the losers (Italy, Spain…).

SaaS of all types, solving pain points of surviving travel companies.

Local travel.

Agile organizations and workforce; niche tourism; new industry standards.

Vaccinations controls, air filters, health insurances.

Cancellation policy will become an integral component. Traditional insurance companies are not what is needed. A new network of insurers for both companies and travelers will appear.

Automatization of back office and customer front end related services

Solutions that incorporate and/or mitigate travel risk factors — financial / health / environmental into the travel decision-making process.

Travel and pharmaceutical partnerships

Q6. What do you think are the previous biggest travel mega trends that make less sense post CV19?

See below in italics some of the representative responses by survey respondents.

The business where the opportunity lay in managing margins based on the assumption of a continuous increase in demand: Oyo with hotels, Sonder with apartments. That is, not being the provider neither the distributor, but a middleman.

Master lease model and revenue guarantees in alternative accommodations.

The alternative accommodation industry will have to do more to build travelers’ confidence for their safety, health and well-being.

Bots, I think people will become more human and want to speak with humans instead of bots (automation will be tools but not for customer service). OTAs not focused on customer care will disappear or they will become aggregators of content, reducing their bill and market share.

Significant reduction in corporate travel — company meetings, customer visits, and group events. Zoom gets richer (more non-verbal communication tools) and becomes an acceptable substitute for a lot of in-person connection.

Low cost long distance.

Tours and activities will be a challenging space as many consumers are likely to feel uncomfortable for some time around crowds. Museums, popular attractions and events will all be more challenging to sell.

International leisure travel.

Tourism growth strictly for economic benefit at the expense of social / environmental impact.

Peer to peer businesses. Travelers will have less money but at the same time will be more cautious about where to stay, eat, etc. First 6 months alternatives methods will have to work hard to give the sense/evidence of full sanitary conditions.

Urban crowded tourism down in favor of travel to open and natural environments.

Customization of experiences. It won’t be seen as core part of the businesses and it will be more difficult in a fast changing environment

Fleets of A380s

Price parity

In summary, these were the challenges and opportunities that seemed to have the most traction in the responses:

Opportunities

- Insurance policies, flexible bookings

- New standards in hygiene, safety, health and well-being

- Travel disruption solutions

- Duty of care

- Domestic travel

- New destinations (less crowded, closer, safer)

- Open spaces, nature

- Customer service/care in crisis time as competitive advantage

- Human customer service

- Anxiety reducing experiences

- Virtual meetings / conferences

- Travel risk reduction solutions

- Alternative transportation

Challenges

- Cruises

- Group travel, tours

- Corporate travel

- Long haul air travel

- Mass tourism destinations

- Urban tourism

- Master leasing models based on constant increases in demand

Thanks to all 65 travel industry respondents who completed this survey. I hope you find these results useful. Share with me any thoughts you might have- would love to hear from you!