Travel Sector Opportunity Matrix

A look at the opportunities and challenges ahead for various travel subcategories (products, players and trends).

If you’re not yet a subscriber of the Travel Tech Essentialist newsletter, sign up below to receive every 2 weeks a newsletter with 10 insights.

In the Travel Tech Essentialist newsletter #45, I referred to a a framework for decision-making in time of change that was proposed by Alex Rampell, GP at Andreessen Horowitz. The matrix has 4 quadrants, two of which reflect potentially good investments and the other two point to potentially bad investments:

Best investments:

Structurally positive means that something has finally caught on—there’s no going back to the older, worse, more expensive alternative.

Ephemerally negative: consumption has been rendered challenging, but there is a lot of latent demand which will be soaked up once activity returns. The key is to make sure the cost structure is aligned to persevere past the ephemerally negative.

Bad investments

Ephemerally positive, under the mistaken assumption that the euphoria for something temporary carries over into permanence. A one time boost as opposed to a long term change of habits.

Structural negative. Negative long term perspective, with no likelihood of improving.

In this matrix, the author placed “work travel” as an example of structural negative (potentially bad investment), and “leisure travel” as example of ephemeral negative (good investment). I mentioned in my newsletter that it would be interesting to have such an analysis done for the travel industry. I asked subscribers to provide their input of which quadrant they would place 26 travel subcategories (private aviation, alternative accommodations, airport tech, TMC, outdoor travel, travel insurance, campers, bus, OTAs, etc…).

In the first two sections of this post, I show the results of this exercise reflecting the opinion of 50 travel tech entrepreneurs, executives and investors who completed the survey. In the third section, I conclude with the travel sector dynamics that I am watching carefully and in which I expect significant activity going forward.

1. Travel Sector Opportunity Matrix

The Travel Sector Opportunity Matrix shows the most frequent opinion for each sub-category. So, for instance, Alternative Accommodation is in the structurally positive quadrant because that was the most frequent opinion among the 50 respondents. The subcategories that have a star (*) mean that they are found in two different quadrants (tie). The green squares (structurally positive and ephemerally negative) are the potentially better opportunities and the red squares (structurally negative and ephemerally positive) are the potentially bad opportunities.

The matrix below is self-explanatory, but here are some observations. The accommodations subcategories -hotels, alternative accommodations- both have positive outlooks. In transportation, there are mixed results, with legacy airlines and private aviation being placed in red quadrants, while low cost carriers, train, and bus are in green quadrants. For cruises, one of the worst impacted sectors in travel, the most common response was that the demand will still be there post-pandemic. Conversely, Campers & Recreational Vehicles has been one of the bright stars in travel during Covid but respondents think that this will be ephemeral. Business travel and traditional TMCs are in a red quadrant, but there is a positive outlook on tech TMCs and trade shows. There is optimism for OTAs but not for traditional travel agencies. There seems to be a consensus that all the progress in touchless technologies are here to stay.

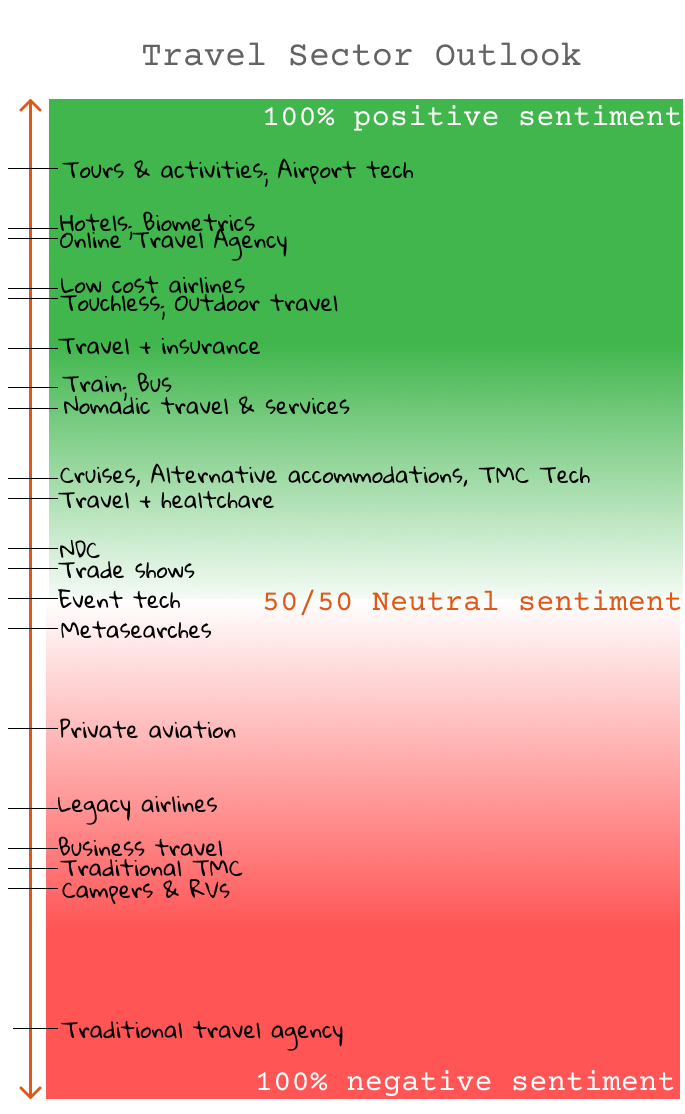

2. Travel Sector Outlook

This next graph reflects the relative level of optimistic or pessimistic opinions for all the subcategories in the analysis. For example, if 100% of respondents placed a subcategory in the red quadrants, it would show 100% negative sentiment (on the very bottom of the line); if 100% of respondents placed a subcategory in the green quadrants, then it would show on the very top of the line with a 100% positive sentiment. So, the higher a subcategory is on the line, the higher the share of respondents that placed it in a green quadrant.

According to the responses, the subcategories with the most optimistic outlook are Tours & Activities and Airport Tech. On the other extreme are traditional travel agencies.

As mentioned earlier, the data reflects the opinion of 50 professionals who work in the travel tech space. It is by no means quantitatively significant, but I believe that it shows insights that are directionally relevant.

3. What I’m looking at

These are some of the dynamics that I’m interested in seeing how they evolve going forward:

Work, education and travel

Work from the office → work from home → work from anywhere. Same applies for education. The future of work and future of education have both been fast forwarded and jumped to the present. They both will have important implications on the travel industry.

Transportation is ripe for disruption

We have seen many changes in the accommodations space, with the emergence of a multitude of new types of accommodations and intermediaries. The largest retailers have moved from being overnight hotel stay specialists to specialists in all sorts of places to stay. We have not seen this level of disruption in transportation. There is a tremendous fragmentation in types of transportation and consumers and this is becoming confusing for consumers. For instance, consumers are not necessarily looking to go from “airport closest to point A to airport closest to point B”; they are looking to get from point A to point B in the most optimum way for their individual criteria, and they are not finding easy answers. If specialized multimodal aggregators (such as OTAs) don’t step up, the likes of Google or Amazon will.

Supplier direct

Still lots of room for improvement in supplier (hotels, airlines…) direct booking. A couple of years ago I saw a report that stated that 52% of OTA visitors went to the hotel website before booking in the OTA. These were potential direct bookers who were underwhelmed by what they saw when they landed in the hotel’s digital presence. Suppliers have improved their merchandising and online booking capabilities in the last years, but there is still a significant upside here. It will be hard for suppliers to effectively compete against retailers in digital real estate (i.e. online marketing), but suppliers can do much more in improving conversion and loyalty.

Retailers shine in complex environments

Retailers such as OTAs should thrive in a world in which products are becoming more complex (cottages, bungalows, shared rentals, etc…), suppliers more fragmented (micro mobility, urban mobility, regional carriers, buses…), and consumers have additional decision-making criteria (payment terms, flexibility, health, insurance…). OTAs are well positioned to bring some order into this potential chaotic environment. But as suppliers step up their game, and to avoid an increasing number of consumers simply using OTAs as a metasearch discovery tool, OTAs will need to give consumers new reasons to continue booking with them, including loyalty programs, subscription programs, price guarantees, cancelation policies and overall flexibility.

Customer service as the new acquisition and retention strategy

Suppliers and intermediaries failed in this pandemic crisis and customers won’t forget. It will take time to rebuild this trust. As the UnderArmor CEO says, trust is built in drops and lost in buckets. Customer service will become a key criteria for consumers for deciding where to book. Where silicon-based intelligence lacks, carbon-based intelligence (i.e. real humans) need to be readily available.

Technology’s third wave comes to travel

Steve Case predicted a few years ago that the next wave of legendary companies and entrepreneurs will be those that are able to transform major “real world” sectors (like health, education, transportation, energy, and food). Covid has accelerated the arrival of the Third Wave to the travel industry. I believe that we will start seeing that some of the fastest growing and largest companies in travel could be defined as insurance, real estate, security, healthcare, IoT, logistics, data, education, retail or aerospace companies as well. It is clear that there are big shifts taking place within society and in a variety of sectors that will lead to rapidly expanding markets for the travel industry.

Travel + finance

Some of the most promising travel companies are insurtech and fintech companies. Examples include Hopper (I recently wrote about Hopper here), Uplift (has raised $695 million in equity and debt), Fly Now Pay Later (landed £35 million in Series A funding in May 2020 and is planning for a £100 million funding package in 2021) and Setoo. We will soon look back in disbelief at the the times when travelers were offered a one-size-fits-all insurance (which no one understood what it really covered) and booked with no peace of mind pricing and with inflexible payment terms.

A new age of startup and corporate collaboration

Silicon Valley entrepreneur Steve Blank (and one of the key individuals behind the lean startup movement) wrote last year (link) that a company’s survival in this downturn can be captured in a simple formula: Survival = (speed of your understanding of the situation) x (the magnitude of the pivots/cuts/lifeboat choices you make) x (the speed of your time to make those changes). A startup can generally do better than a larger company in all the variables in this equation. Corporates are better at executing “business as usual”, but business as usual has meant “no business” recently. What was previously “not urgent” could have become an immediate imperative as a result of this pandemic. Think of flight disruption and rebooking solutions as an example. With downsized organizations and a need to innovate in new areas outside of their core businesses, corporates will likely need to increase their level of collaboration with startups. The pandemic may have tilted the corporates’ build vs buy tradeoff towards the buy side.

Pandemic-native startups

More than half of the largest and most successful companies today were born either in a bear market or recession. Many of today’s travel leading brands were born in the 2008 financial crisis. Such is the case of Airbnb, GetYourGuide, Vacasa, SilverRail, and Adara among others. In the previous paragraph I referred to the importance of pivoting and adapting to the new environment. What’s even better than pivoting is being a pandemic-native startup, born onto this environment with a product, business model and market orientation that is 100% adapted to the new conditions.

Experience economy - Immersive museums and experiential centers

The emerging industry of immersive museums and experiential cultural centers will expand and grow post pandemic, offering a new alternative for both fly-in travelers as well as local and regional tourists.

Here to stay

All events and trade shows will be hybrid.

There have been massive improvements in the traveller experience brought by touchless and biometric technology. If you haven’t travelled through an airport recently, you will be pleasantly surprised next time you fly.

New travel categories such as campers and RVs might have had a one-off boost, but there will be a long term positive impact. A large number of new consumers have discovered this vacation option and a share of them will convert to repeat customers.

Same applies to new destinations. There is a long term positive impact in the diversification of destinations and leisure options that will stay post pandemic.

I would love to hear from you on the results and outlook expressed in this post. And if if you want to add your input to Travel Sector Opportunity Matrix, you can do so here.

And please, if you’re not yet a subscriber of the Travel Tech Essentialist newsletter, sign up below to receive every 2 weeks a newsletter with 10 insights.

Thank you for this matrix. It confirms to me that I am on the right track with the website www.ethik-hotels.com, a platform that facilitates access to sustainable tourism for all. We refer to responsible accommodation all over the world and local incoming agencies for those who wish to travel better but do not wish to organise their trip alone.

I will take this for granted: "What was previously “not urgent” could have become an immediate imperative as a result of this pandemic"